The Solvency II regulatory framework is built on a 3 pillars approach:

The Solvency II regulatory framework is built on a three-pillar structure on a risk-based approach that aims to enable a full assessment of the “overall solvency” of insurance and reinsurance undertakings through quantitative and quantitative measures:

Pillar 1: this pillar sets the qualitative requirements (asset liabilities valuation, capital requirements)

Pillar 2: this pillar sets the qualitative standards (governance, risk management, Own Risk and Solvency Assessment – ORSA)

Pillar 3: this pillar sets public disclosure and supervisory reporting

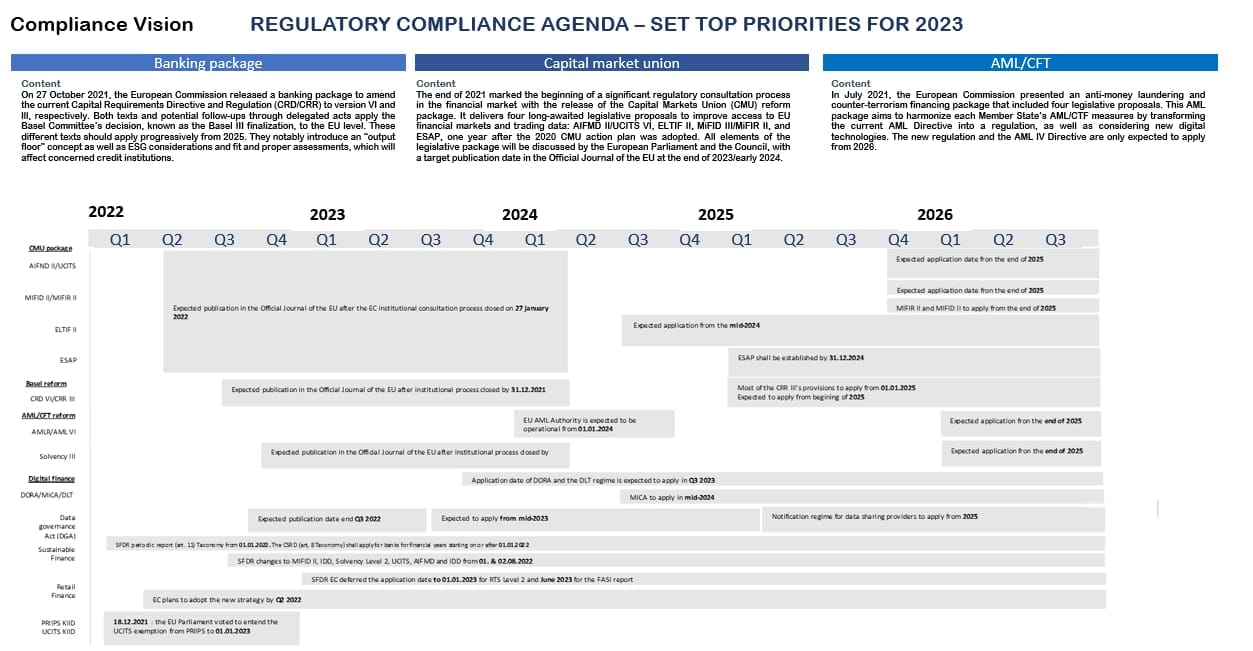

Another objective is to improve the quality of supervision and standardize the rules, especially regarding ongoing compliance with prudential rules, cross-border insurance businesses, and insurance groups. Finally, climate and systemic risk considerations are introduced to ensure these risks are better managed and supervised, mainly through long-term climate change scenario analysis. The 2020 Solvency II review has suffered delays due to the COVID-19 crisis, with stakeholders willing to ensure that related economic and financial observations are considered. Given the next steps required for negotiating the final legislative texts by the European Parliament and the Member States, transposition of the revised Directive into local law, and in parallel amendments to Delegated Acts, the revised Solvency II regime is not expected to enter into force before 2025.

Moreover, the EC proposes phasing-in more impactful measures to avoid disruptions and ensure a smooth transition. These new measures will significantly affect insurers and reinsurers, especially their solvency ratios, on their capitol charge and their own funds’ valuation. Undertakings should be prepared to review their strategy and calculation models, particularly those with long-term liabilities, and adapt their systems and internal processes to meet the new reporting and disclosure requirements. It is worth noting that these rules are still up for negotiation and may be changed. Undertakings should remain vigilant to developments and the final measures negotiated and ensure their implementation process is sufficiently flexible to handle potential changes.

Courses:

1. The 3 Pillars of Solvency II

2. Solvency II main features

3. Governance of Solvency II

4. Solvency II capital requirements

5. Solvency II market risk

6. Solvency II counterparty risk

Curriculum

- 1 Section

- 6 Lessons

- Lifetime

Download reportCompliance Academy Guide

Download reportCompliance Academy Guide